DIY Investor Magazine

/

March 2014

10

BY BEN THOMPSON

DIRECTOR, BUSINESS

DEVELOPMENT, LISTED

PRODUCTS & LYXOR ETF

CONSTRUCTING AN ETF PORTFOLIO

Exchange Traded Funds, or ‘ETFs’ as they are known,

are leading the charge in a new democratic world of

investment where investors are increasingly taking

charge of their own portfolio.

Why? Firstly because they are simple to trade. Just like

regular shares, ETFs can be purchased through a UK

stock broker using a share dealing account, ISA or SIPP.

The second reason is diversification. ETFs are

intrinsically diverse. For example, instead of building

your own portfolio of UK equities, and paying costs

and fees on each one, you can purchase a single ETF

that provides exposure to the top 100 UK companies

through the FTSE 100 Index.

Not only are the vehicles themselves diverse, but

with a product range spanning different market

sectors, regions, themes, commodity baskets or fixed

income strategies, and the whole risk spectrum from

government bonds to single country emerging markets,

ETF investors can easily create a well diversified core

portfolio. Furthermore, with both income paying

(distributing) ETFs and growth (capitalising) ETFs

available, they can capture both growth and income.

ETFs can also be used tactically to take advantage

of short term trends. The combination of core and

satellite allocations means that investors can build a

portfolio to suit their specific views and investment

budget. Small portfolios can be built with a handful of

ETFs, and larger portfolios with very specific exposures

can achieve even greater diversification. The third

major factor is cost. Unlike actively managed funds

where you are buying the skills of a ‘Manager’, with

ETFs you are simply buying a passive investment that

tracks a benchmark index.

As such, ETFs are significantly cheaper and Total

Expense Ratios (TERs) typically range between 0.15%

and 0.85% per year. This TER is the annual charge that

includes costs such as custody fees, marketing costs

and index licensing costs. On top of this, investors will

be charged a brokerage fee in the same way as when

buying shares. Importantly though, the TER is not a

true measure of the Total Cost of Ownership (TCO).

Although all ETFs share the same aim – to track an index

as cost effectively and precisely as possible – some do it

much better than others. Tracking difference and tracking

error are two measures that describe how precisely and

consistently the ETF tracks its benchmark. As anything

less than the index performance is a cost to you, it is

important to look at these variables. The bid/ask spread

will also impact performance as the difference between

buy and sell price is key to your trading cost.

As with any investment product, ETFs carry a number

of risks. Most ETFs are index tracking funds, meaning

the performance of an ETF will rise and fall with the

underlying index which may be complex and/or volatile,

exposing investors to market risk. Investors’ capital is

at risk, and you may not get back the amount originally

invested.

Investors may be exposed to counterparty risk resulting

from the use of securities lending in physical ETFs, or

from the use of an OTC performance swap with an

investment bank for synthetic ETFs. If the index or the

constituents of the index are denominated in a currency

different to that of the ETF, investors are exposed to

currency risk from exchange rate fluctuations.

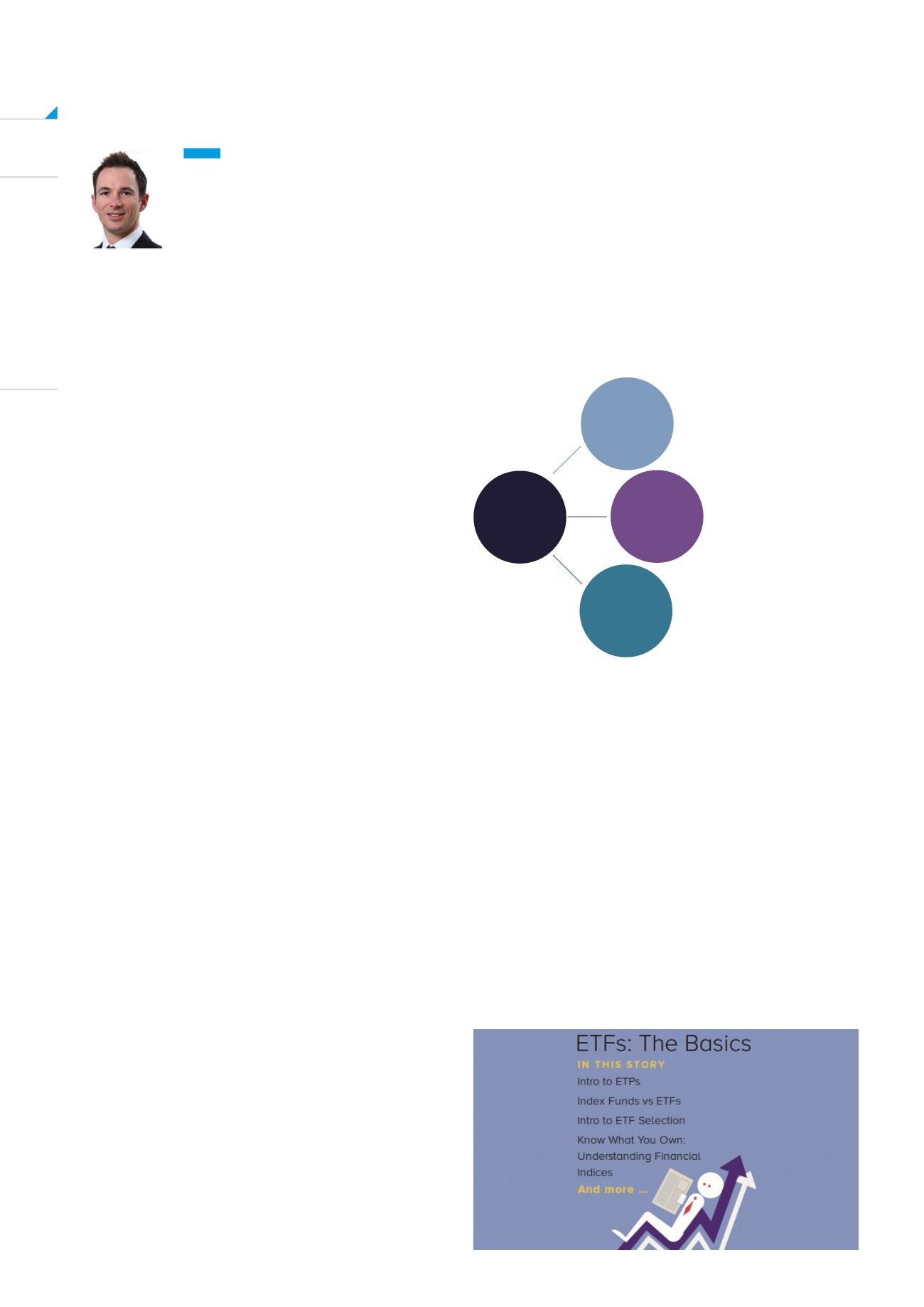

TRACKING

DIFFERENCE

How close is the performance

of the ETF to the Benchmark?

How accurately does the ETF

track the Benchmark Index?

What is the spread between the

Buy (Ask) price and sell (Bid) price?

TRACKING

ERROR

TRUE

PERORMANCE

LIQUIDITY